The HSA opportunity clients miss

Odds are your clients are struggling with higher insurance costs and worried about incurring any future medical bills. Here’s one option advisors can help them explore: health savings accounts. These accounts, which are offered in combination with high-deductible health insurance plans, provide a unique opportunity for clients to save. Better still, they afford triple tax advantages.

Widespread confusion about how these accounts work however can keep clients from establishing HSAs or taking full advantage of them. Unfortunately, advisors are often at sea as well, particularly when it comes to helping clients establish their own account outside of an employer.

“In my experience, a lot of planners focus on investments rather than insurance, so unless they themselves are purchasing individual health insurance or have lots of clients who do, they’re usually not very familiar with independent HSAs and don’t know in-depth details about them,” says financial planner John Chan with Alamo Insurance and Wealth Management in San Antonio, Texas.

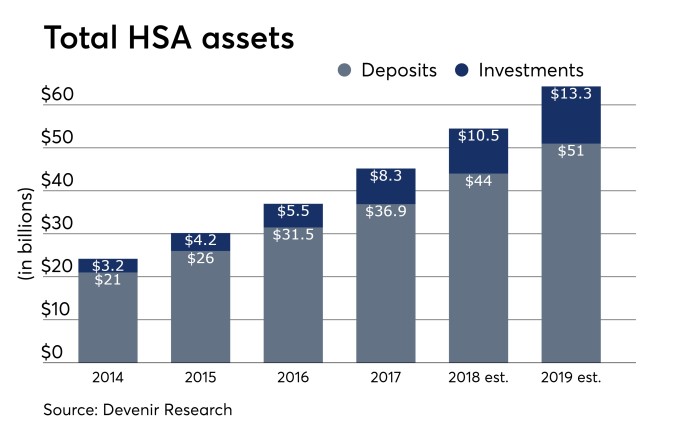

Because HSA savings enjoy triple tax advantages: contributions are tax-deductible, earnings accrue tax-free and tax-free withdrawals can be made for qualified medical expenses, failing to help clients establish their own can be a big missed opportunity.

“Advisors I’ve spoken with know the basics of an HSA, but I feel many advisors under stress HSAs with clients,” adds planner Stephen Jordan with Cyr / Woertz Financial Group in Peoria, Illinois. “I think it is a really important tool, especially as we don’t know what medical costs or Medicare will look like in the future.”

But advisors who do have a solid grasp on HSAs can build client loyalty, which, in turn, means referrals.

“Most clients did not know HSAs existed, but were excited they could get an additional tax deduction,” says Chan. “Many did go through with opening their own HSAs and have max funded them. They felt it was very beneficial and appreciated that I brought the account to their attention.”

Figuring out HSA eligibility: First, clients will need to confirm that their health insurance plan can be paired with an HSA. For many, this will be fairly obvious, as often high-deductible plan names will include HSA in the title. But if it is unclear, clients should check with their insurer.

“Try to discourage people from making such a determination their own,” says Roy Ramthun, president and founder of HSA Consulting Services.

To qualify as a high-deductible health plan that can be used with an HSA, the IRS says the plan must offer a minimum annual deductible of $1,350 for individuals or $2,700 for families, as well as a maximum annual deductible of $6,650 for individuals and $13,300 for families.

Clients cannot have any other health insurance coverage, be enrolled in Medicare or be covered by another plan, say through a spouse, Ramthun says. And they cannot be claimed as a dependent on someone else’s tax return. If they’re covered by a high-deductible health plan that’s already paired with a flexible spending account or health reimbursement arrangement, they typically will be unable to contribute to an HSA.

Encourage clients to do this check as soon as they’ve joined a high-deductible plan. Any medical expenses they accumulate prior to opening the HSA will not be reimbursable, even if they were on an eligible health insurance plan at the time, says Paul Fronstin, director of the Employee Benefit Research Institute’s health research and education program.

Where to open the HSA: Clients can pick from any one of the hundreds of financial institutions that offer HSAs to set up an account with. But not all HSA providers are created equal; huge variations between interest rates, fees, and investment options exist.

How your client intends to use the HSA will have a huge impact on which features should take top consideration when recommending a provider. If they will be using it to pay current medical costs, account maintenance fees should be the main concern. Other items like a debit card and easy online bill pay are also worth looking into, Ramthun adds. If instead, the HSA will be used an investment vehicle to save for future medical expenses in retirement, then the focus shifts to the plan’s investment menu, the underlying managers and fund fees.

An analysis by Morningstar of the 10 largest HSA-plan providers found that Alliant Credit Union was the best option for clients using an HSA for current spending. It also recommended SelectAccount and The HSA Authority because, like Alliant Credit Union, those providers also offer checking accounts without monthly maintenance fees.

For those looking to invest HSA savings, Morningstar found that HealthEquity was the one plan offering “a well-designed investment menu, strong underlying managers, and attractive fees.” But it also recommended Optum Bank, The HSA Authority and Bank of America. All four of those plans had at least two of the three following features, Morningstar says: a well-designed investment menu, solid quality underlying managers and below-average fees.

Only The HSA Authority was recommended as both a spending and saving vehicle, according to Morningstar.

Funding the HSA: Because a client’s employer is not associated with the HSA, they may need to ask HR if it is possible to have a portion of their pay or bonuses directed to it, or, if they can’t do that or are self-employed, they will need to take a more active role in funding the account.

For 2018, those with individual coverage can save a maximum of $3,450 in their HSA. For those with family coverage, the contribution limit jumps to $6,900. Clients who are 55 or older by the end of the year can sock away an additional $1,000.

If your client joined a high-deductible plan during the year, they can still contribute the maximum as long as they had coverage by December 1, under what’s known as the last-month rule. But taking advantage of that rule comes with a big caveat: clients must remain on a high-deductible plan for all of the following year. Failing to do so may mean they’ll have to claim “excess” contributions as part of their taxable income and pay an additional 10% penalty tax on that sum.

Remember all funding limits are related to tax filing status too, meaning that while spouses can each have their own HSA, the maximum remains unchanged if they file a joint tax return. For instance, a husband can put $4,000 into his HSA this year, but that means his wife can only contribute $2,900 to hers, so as a family, they still remain under the $6,900 limit.

For families with adult children still on the family health plan but who file their own independent tax return, this presents an opportunity to fully fund two HSAs connected to the same insurance coverage, says Ramthun. So, a client and their adult child can each open an HSA and each stash the full $6,900 in it this year. Happy news for broke children: the funding can come from someone beside the account owner. Bad news: parents can’t use their HSA funds to cover that independent child’s medical costs.

“Contributions can be put in as a lump sum or be spread out over the course of the year,” Ramthun says. “But if they want the tax deduction, they need to make sure the money is in the account before the April tax deadline, though I urge people not to wait that long. If they want to wait to see how much medical expenses they actually incurred and use it as a cash account, they should still put the funds in by the end of the year.”

All contributions made to an independently-opened HSA are still deductible from taxable income, even if a client doesn’t itemize. The tax break just won’t be realized until a client completes their tax return and files IRS form 8889. That said, workers will typically lose out on FICA tax benefits on their contributions, adds Fronstin.

If you already have an HSA: Clients who already have an HSA but then join an employer that offers a different HSA, have two options. They can keep both accounts or close the one they opened independently and move the funds to the work-related HSA.

They should not, however, opt out of the work-related account, advises Ramthun. They’ll need to leave it open to receive any employer HSA contributions.

Rather, if a client wants to keep the original HSA they opened, they should opt to do a trustee-to-trustee transfer once or twice a year, Ramthun says. “You can move the money between HSAs as often as you want, but I would limit it as there can be fees involved.” Also, be careful not to “roll” the money over. Taking the money out of an account and into your possession only to deposit it again in another account, must be done in 60 days and can only be done once a year, just like with an IRA.